The Great Debasement.

Why I'm Betting that Governments Will Inflate Away Their Debt.

Disclaimer: This is NOT financial advice or a recommendation to buy or sell securities. We have NOT been paid or compensated for this article, but we are shareholders of some of the companies mentioned and as such are extremely biased. There are a lot of calculations contained below and it’s likely errors have been made. Please complete your own due diligence and read our full disclaimer here.

Day 2 of 30 days of daily content.

Nothing ever really happens. That's been the unspoken contract of modern life. Markets wobble, politicians bluster, headlines scream, and then everything goes back to normal. COVID stress-tested that assumption. What's coming next will break it. I believe the next two to three years will produce the most significant global economic shift since World War II. The most significant shift in my lifetime. Not a recession. Not a correction. A restructuring.

But what's unfolding right now is different. Something will and is happening. There won’t be one news story to sum it all up and make sure your eyes and ears are open. This isn’t a single event. It's structural. Meaning: the forces driving this aren't temporary shocks that governments can stimulus-spend their way out of. We're talking about a convergence of record sovereign debt, a geopolitical energy crisis, the unwinding of globalization, and the early stages of what I believe is a deliberate (or at the very least, tolerated) inflationary regime designed to quietly erase government obligations. Each of these things alone would be significant. Together, they're reshaping the global order.

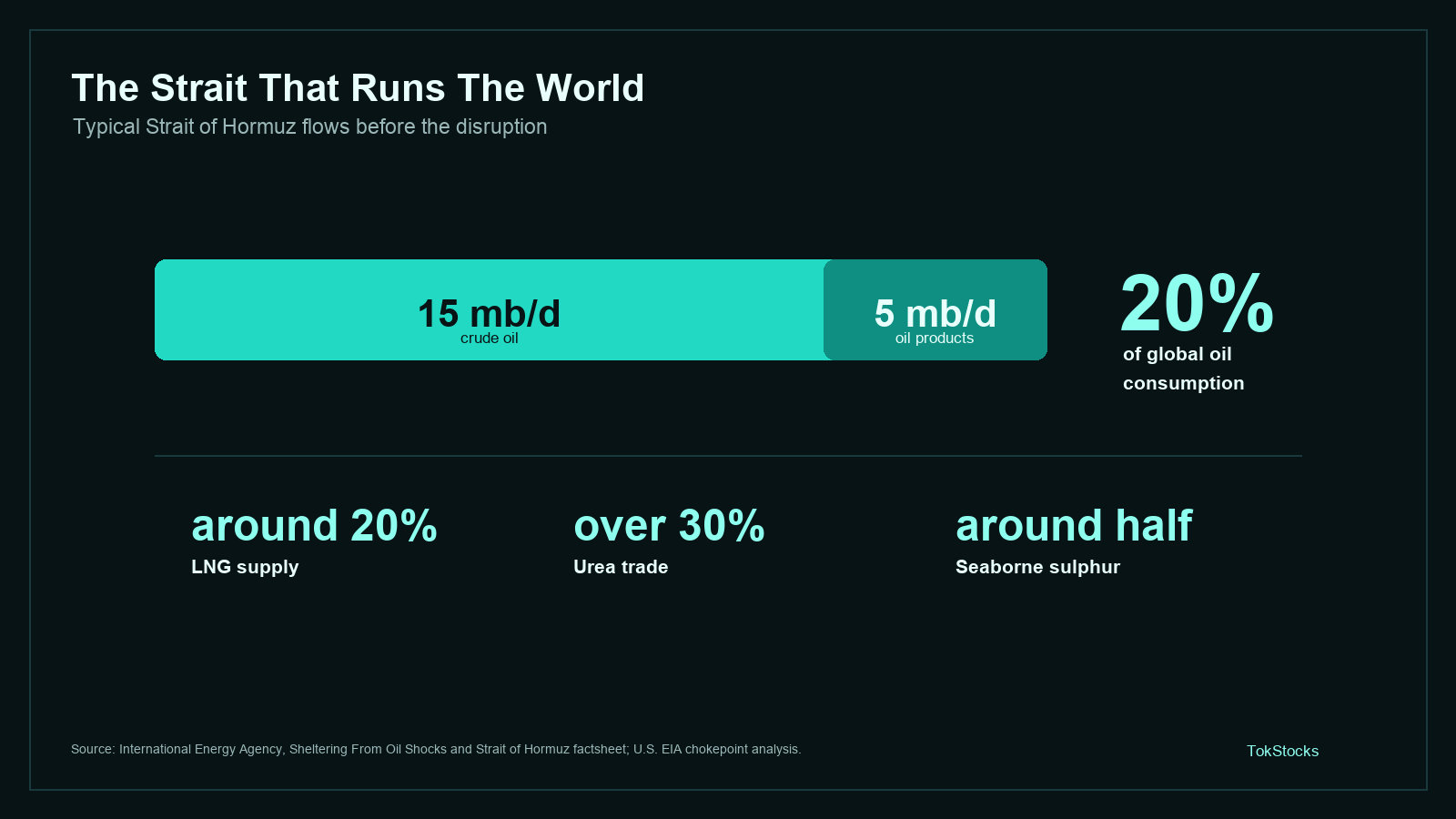

The Strait That Runs the World

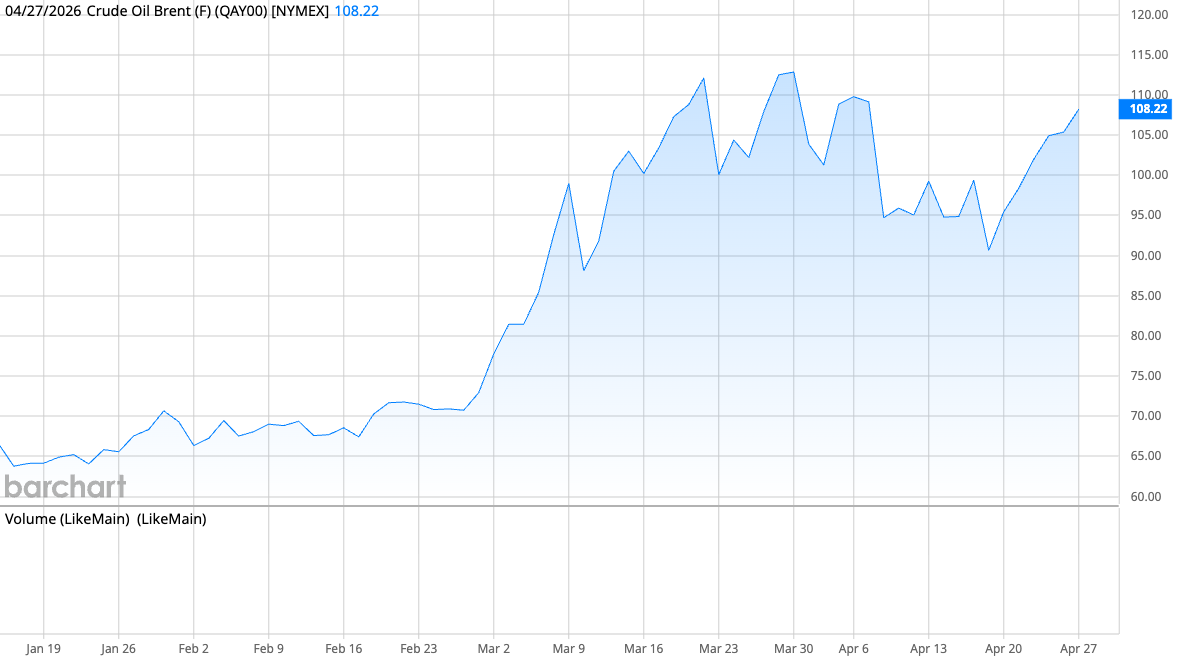

I know. Sick of hearing about this. But we have to start with what’s right in front of us. The Strait of Hormuz, a narrow channel barely 33 kilometres wide at its tightest point, carries roughly 20% of the world’s oil consumption. The IEA (International Energy Agency) has called the current disruption the “largest supply disruption in the history of the global oil market.” Crude flows through the Strait have plunged from around 20 million barrels per day to a trickle. Brent crude hit $126 a barrel at its peak (about $109 today), roughly $60 above pre-conflict levels.

The domino effects are only beginning. We’ve felt it at the pump. But the second and third order effects, the ones that hit manufacturing, transport, agriculture, tourism, and basically everything else, those haven’t fully landed yet. Existing inventories are being drawn down. As they are being replenished at $100+ oil, that cost gets passed through the entire economy.

This is how you get stagflation: rising prices colliding with slowing growth. Bank of America has already revised its base case to oil at $100 for the rest of 2026 and used the phrase “mild stagflation.” The IMF has cut global growth forecasts. Deutsche Bank and Oxford Economics have both flagged rising recession risk.

And here’s why stagflation is particularly useful if you’re a government sitting on $39 trillion in debt: inflation erodes the real value of what you owe, while stagnant growth gives you political cover to keep rates suppressed. You can’t hike aggressively into a slowing economy. The central bank’s hands are tied. Real interest rates stay negative. And your debt quietly melts. It’s the financial repression playbook, and the conditions are assembling themselves almost too perfectly.

The Numbers Don't Lie, But Governments Do

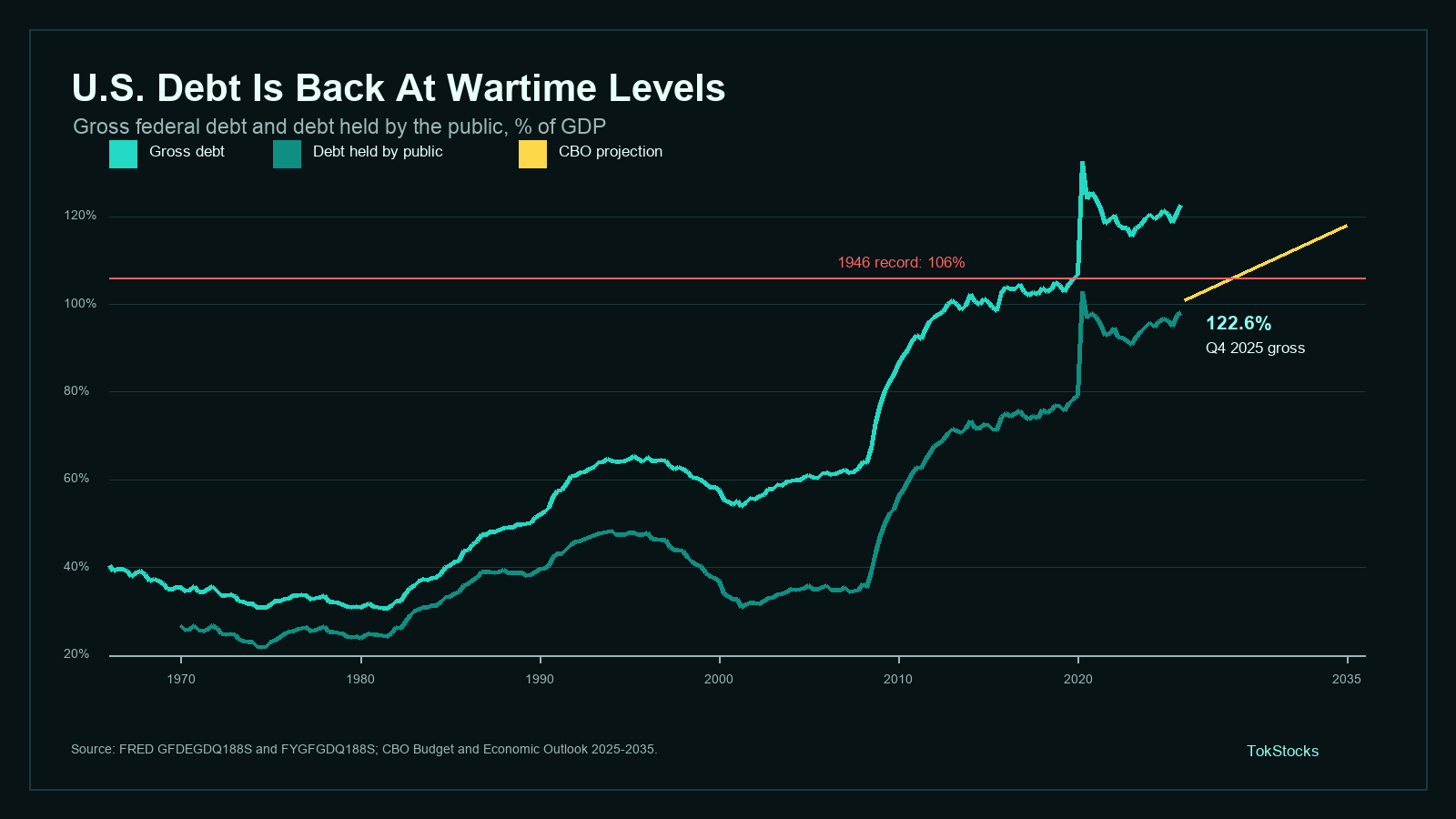

Global public debt hit $100 trillion in 2024. The IMF (International Monetary Fund) pegs it at 93% of global GDP, heading toward 100% by decade’s end. That’s WWII territory. We’re carrying wartime debt loads…and some are still wondering why we’re having more global conflicts? History seldom repeats but it often rhymes. Despite not being old enough, I’m spotting a pattern.

The US alone owes nearly $39 trillion. There are two ways to measure this against the economy, and both tell the same ugly story. Gross federal debt (everything the government owes, including what it owes itself through trust funds like Social Security) sits at roughly 123% of GDP. Debt held by the public (the portion owed to actual investors, foreign governments, and bond markets, which is the number the CBO (Congressional Budget Office) uses for projections) is at 100% of GDP today. That public-facing number is projected to hit 118% by 2035, smashing through the post-WWII record of 106% set in 1946. No matter how you slice it, every measure of US debt is at or above wartime highs and accelerating.

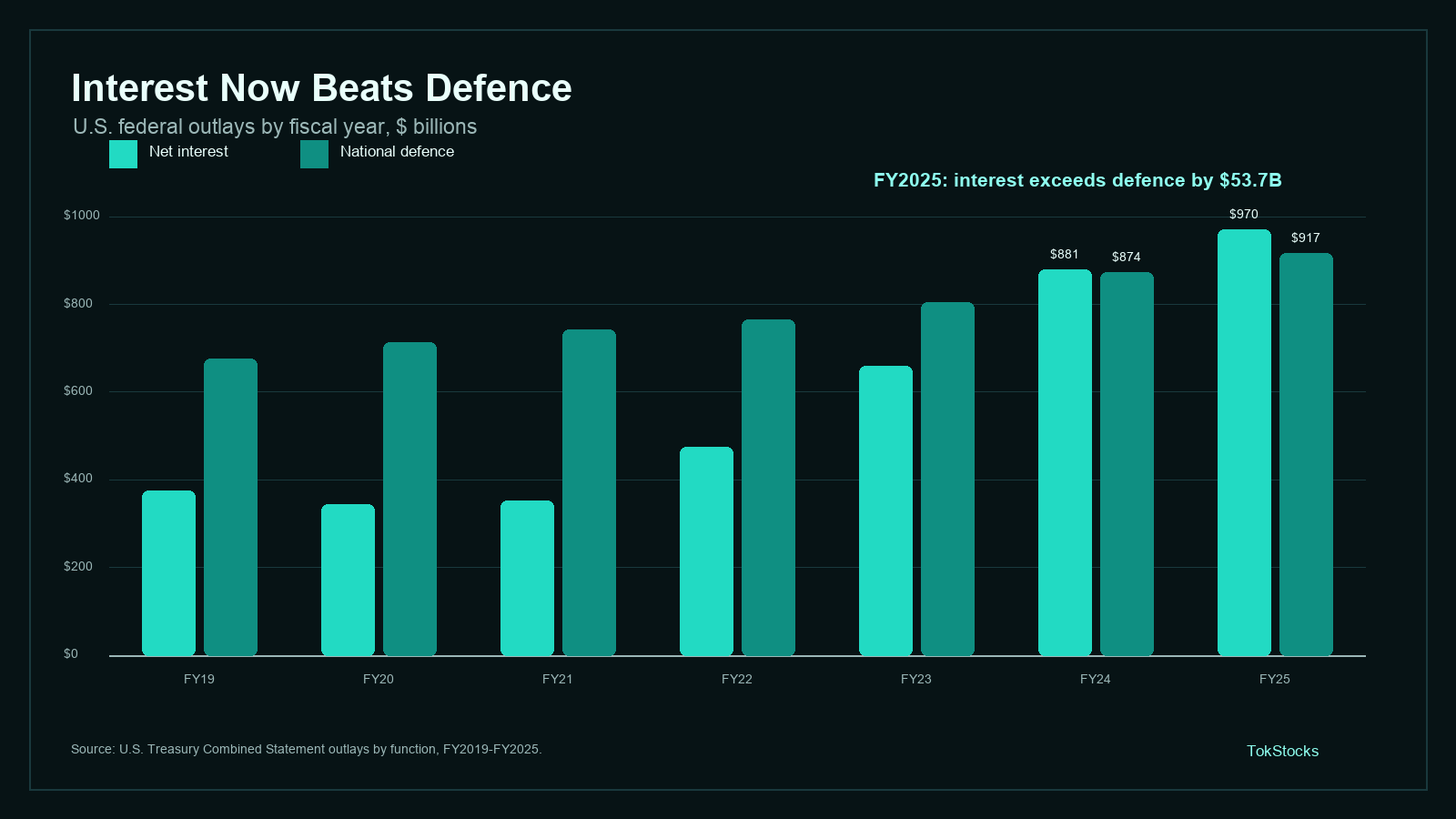

And here’s the detail that should make your stomach turn: in FY2025, the US government spent $970 billion on interest payments alone, while national defence outlays came in at $917 billion. For the second straight year, America spent more servicing its debt than defending itself. That gap is widening, not closing.

The Playbook: Financial Repression

Governments have four options to deal with this debt: grow out of it (good luck), tax their way out (political suicide), default (nuclear option), or inflate it away. Guess which one requires no vote, no announcement, and no accountability?

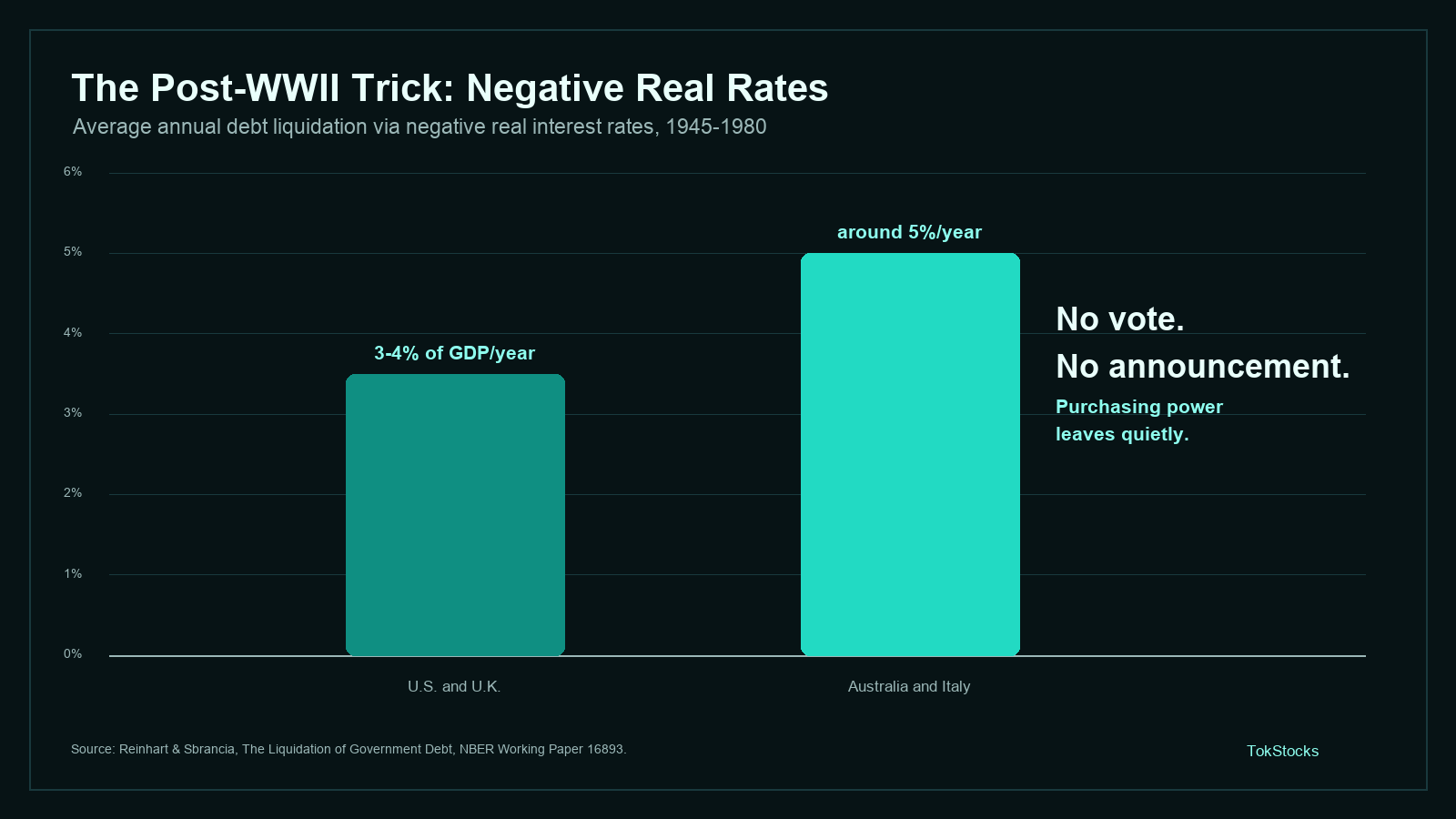

This isn’t speculation. It’s history. After WWII, the US debt-to-GDP ratio was 106%. By 1974 it had fallen to 23%. They didn’t cut spending. They didn’t raise taxes dramatically. They ran what economists call “financial repression”: cap interest rates below inflation, force banks and pension funds to hold government bonds, close the capital borders, and let inflation quietly do the work.

Reinhart and Sbrancia’s landmark research quantified it precisely: negative real interest rates liquidated US and UK government debt at a rate of 3 to 4% of GDP per year from 1945 to 1980, and about 5% in Australia and Italy. Real rates were negative roughly half the time during that period.

The Penn Wharton Budget Model projects that simply raising the inflation target from 2% to 3% would reduce the real value of federal debt by 7% by 2051. No spending cuts needed. No legislation required. Just let the purchasing power of your savings erode. Slowly. Quietly. Like a tax nobody voted for.

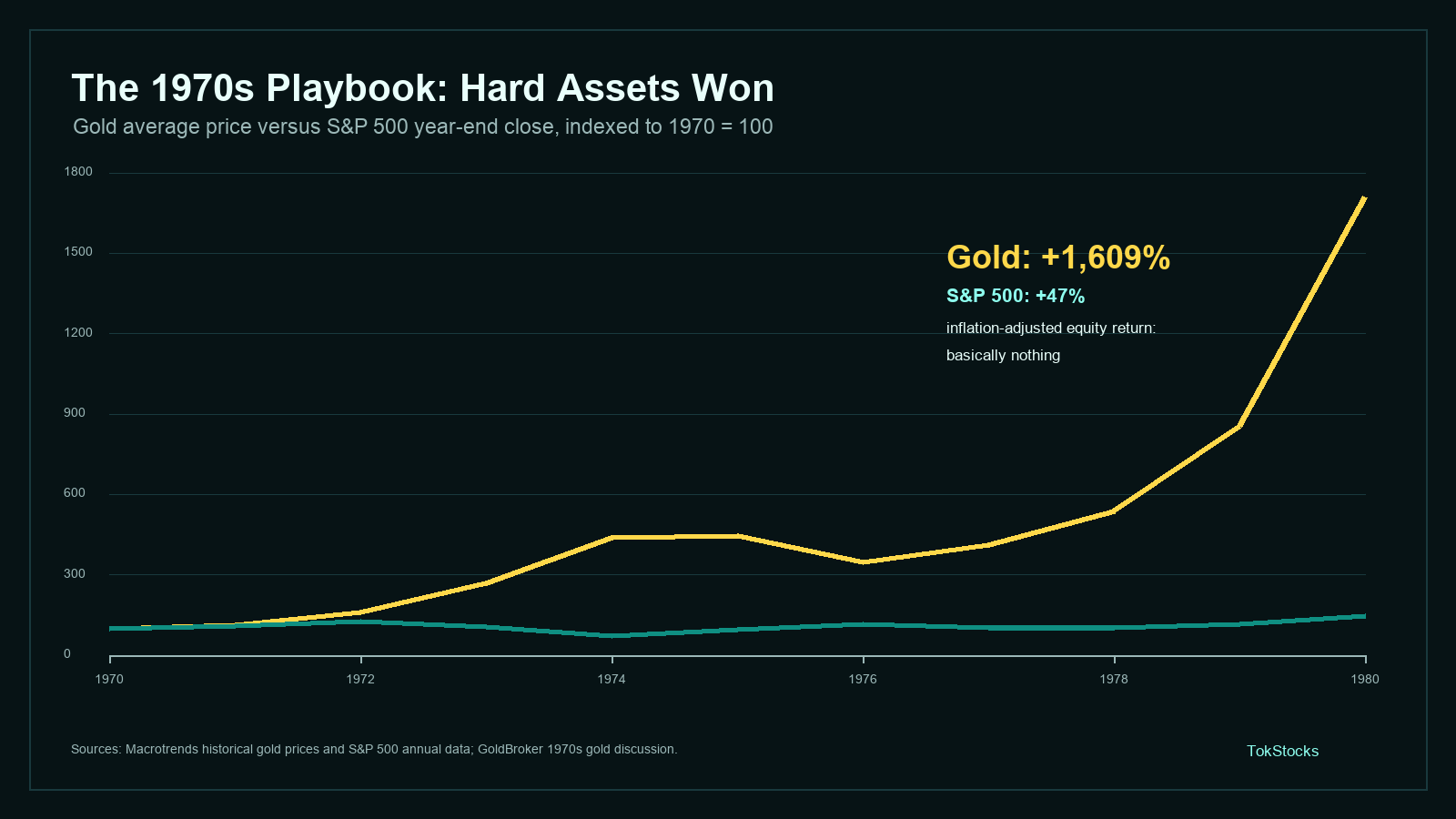

The 1970s Playbook: Hard Assets Win

Last time we were here, gold went up 1,608% between 1970 and 1980. The S&P 500 returned roughly 48% nominal over the same period, which after inflation was approximately zero. Real return on stocks: nothing. Real return on gold: life-changing.

What I'm Doing About It

This is the cornerstone of my investment thesis right now. If governments choose inflation (and history says they probably will), hard asset miners are the trade. Not all of them. The ones with access to domestic energy, low costs, and real production. The kind of companies that benefit from rising commodity prices without getting destroyed by rising input costs.

The world is repricing sovereignty. Energy, metals, defence. The globalization unwind is not a theory. It’s happening in real time, and the assets that performed during the last era of financial repression will perform again.

I don’t think the Great Debasement is coming. I think it’s already here. The debt is too large to repay honestly. The political will to cut spending simply doesn’t exist (remember DOGE???). And the playbook for what comes next, in my mind, has already been written, tested, and proven across centuries of sovereign history. Most times governments have found themselves in this position, they’ve chosen the same door. I don’t believe this time will be different.

And if I’m right, the commodity bull that follows won’t be a blip. It will be generational. The kind of cycle that mints fortunes for those who see it early and punishes everyone who assumes the old rules still apply. We’ve been in this bull for a few years already but I believe we’ll see a new leg up begin.

I’m continuing to build a concentrated portfolio around this thesis and I’ll be sharing it here on TokStocks: the specific names, the reasoning behind each position, and how I’m thinking about sizing and risk. This to me is the trade of the decade. I intend to be positioned for it.

This is not just market volatility. It is proof that the global economy is still fragile by design overexposed to a few critical nodes.

As long as the world depends on narrow energy chokepoints, every conflict has the power to become a global economic shock.

The real solution is not predicting crises better. but building a system where crises have less power to disrupt everything at once.

Brilliantly written, great numbers, rock solid thesis...